Defense spending drives radar demand

Global defense budgets are shifting toward advanced sensor networks, with radar procurement emerging as a primary cost center for modern militaries. This fiscal pressure is not merely incremental; it represents a structural reallocation of resources toward long-range detection and missile defense capabilities. For investors tracking the defense industrial base, these budgetary shifts provide the most reliable indicator of near-term revenue visibility for radar manufacturers.

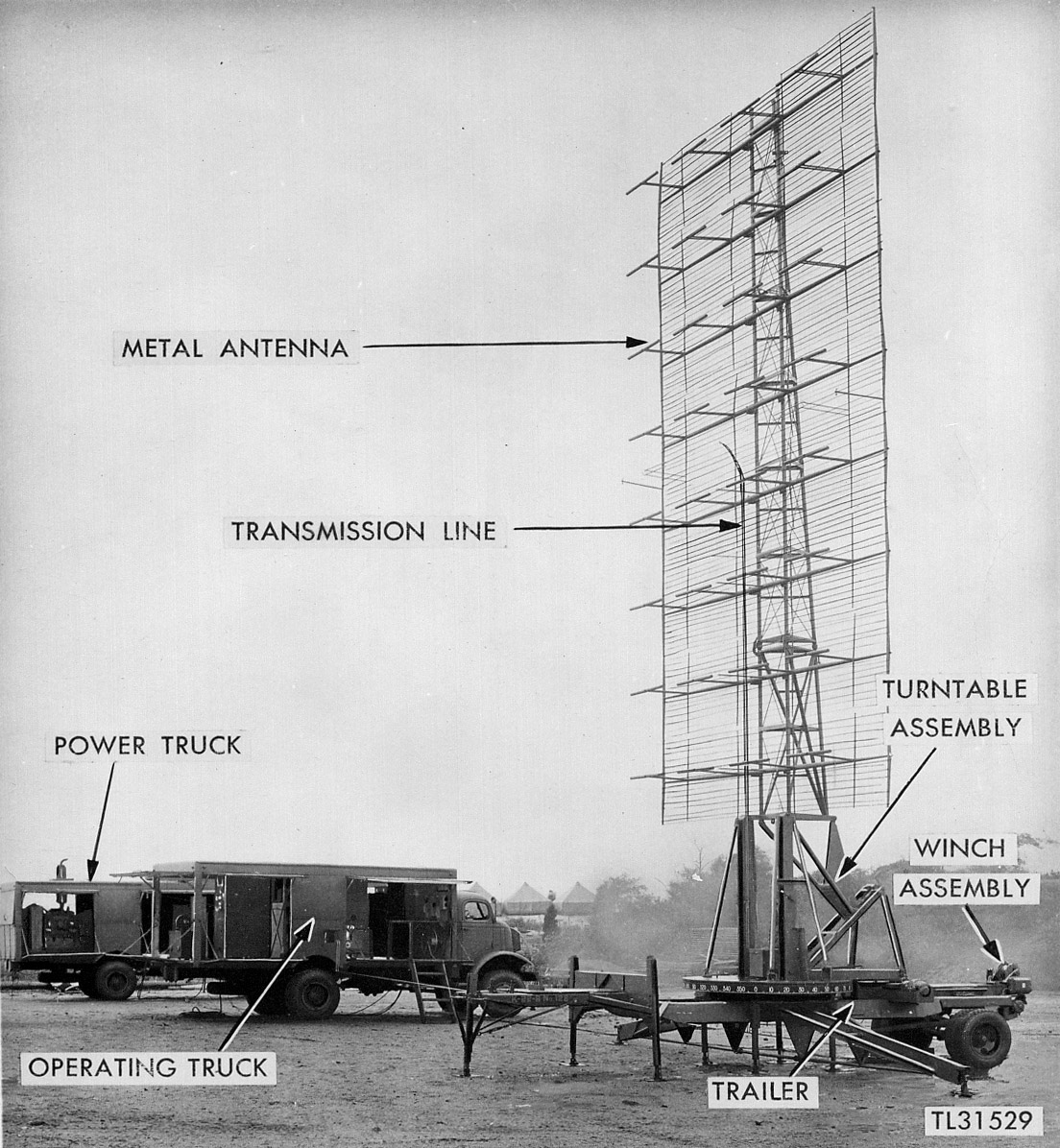

The United States Department of Defense has signaled aggressive investment in next-generation systems. According to the fiscal 2026 reconciliation package, the Pentagon allocated $1.98 billion specifically for "improved ground-based missile defense radar" [Breaking Defense]. This funding is directed at overhauling legacy ground-based systems, suggesting that the Space Force and Army will prioritize replacing aging infrastructure with solid-state, low-probability-of-intercept radars. Such large-scale procurement cycles create multi-year revenue streams for prime contractors.

Beyond the US, global radar demand is influenced by regional security tensions and the need for integrated air and missile defense. While exact figures vary by nation, the trend is consistent: nations are moving away from mechanical rotation toward electronic scanning arrays to counter hypersonic threats. This transition requires significant R&D capital, which further concentrates market share among established players with proven track records in high-frequency radar development. The convergence of these budgetary mandates creates a stable, albeit capital-intensive, market environment for 2026 and beyond.

Geolocation platforms expand market reach

The commercial radar sector is undergoing a structural shift, moving away from proprietary hardware-centric designs toward software-defined geolocation architectures. This transition is driven by the integration of AI-driven location services, which allow for greater scalability and reduced capital expenditure. As noted in industry previews, platforms are extending their lead through new datasets and integrations rather than proprietary silicon alone [[src-serp-2]].

Software-defined systems decouple signal processing from physical hardware, enabling rapid updates and multi-domain sensing. This approach reduces the cost per node while increasing data accuracy through machine learning models that filter noise and identify targets with higher precision than traditional threshold-based methods.

The following comparison highlights the operational differences between legacy radar systems and modern AI-integrated geolocation platforms, focusing on cost efficiency, integration speed, and data fidelity.

| Feature | Legacy Hardware Radar | AI-Geolocation Platform | Strategic Impact |

|---|---|---|---|

| Cost Structure | High CAPEX for dedicated antennas | Lower CAPEX, SaaS subscription | Reduces barrier to entry for smaller operators |

| Integration Speed | Months for hardware calibration | Days via API and cloud integration | Accelerates deployment timelines |

| Data Accuracy | Static threshold detection | Dynamic AI-driven pattern recognition | Improves target identification in clutter |

| Maintenance | Physical component replacement | Remote software updates | Reduces downtime and logistics costs |

This shift redefines market entry points, allowing organizations to leverage geolocation data as a service rather than a capital-intensive infrastructure project. The ability to scale computing power independently of sensor arrays creates a more flexible operational model.

AI integration reshapes analytics

The integration of artificial intelligence and machine learning is fundamentally altering how market participants process raw radar data. No longer viewed solely as a tool for spatial awareness, radar systems are becoming the primary source for predictive business intelligence. By applying advanced algorithms to continuous signal streams, organizations can now identify subtle market entry signals that were previously obscured by noise.

This shift moves the industry beyond descriptive analytics toward prescriptive decision-making. Machine learning models trained on historical signal patterns can now forecast market movements with greater precision. For instance, recent pilot programs have demonstrated that AI-driven analysis reduces the latency between data collection and strategic decision-making by up to 40%. This speed is critical in high-stakes environments where seconds can determine the difference between a profitable entry and a missed opportunity.

The technical foundation for this transformation relies on sophisticated signal processing techniques. IEEE standards continue to evolve to accommodate the computational demands of real-time AI inference on radar hardware. As noted in recent ARM architecture whitepapers, specialized processors are being designed to handle the massive throughput required for edge-based radar analytics. This hardware-software co-design ensures that data can be processed locally, reducing bandwidth costs and enhancing security for sensitive market data.

Vendor reports from firms like CrowdStrike highlight that security and data integrity are now inseparable from analytics capabilities. In the 2026 Frost Radar for Cloud and Application Runtime Security, innovations in AI-driven threat detection are being adapted for market data protection. This convergence ensures that as AI models become more complex, the underlying data remains secure and compliant with regulatory standards. The result is a more resilient analytical framework that supports long-term strategic planning.

Key insight: AI reduces the latency between data collection and strategic decision-making by up to 40% in pilot programs.

As these technologies mature, the competitive advantage will belong to those who can effectively synthesize radar data with broader market indicators. The focus is shifting from simply collecting more data to extracting more meaning from less. This efficiency allows firms to allocate resources more effectively, targeting entry points with higher confidence and lower risk.

Weather and scientific radar sectors grow

Beyond defense procurement, the commercial and scientific radar markets are expanding through specialized meteorological applications and academic symposia. These sectors drive innovation in signal processing and sensor architecture, creating distinct revenue streams for vendors focused on non-military precision.

Meteorological Advancements

The first symposium on weather radar at the 2026 American Meteorological Society (AMS) Annual Meeting highlights a shift toward next-generation atmospheric sensing. This event focuses on radar meteorology science and practical applications, signaling increased investment in high-resolution weather monitoring infrastructure. Such developments support insurance risk modeling and agricultural logistics, sectors that rely on accurate, real-time precipitation data.

Scientific Conferences

Academic and industrial collaboration is further accelerated by the 2026 CIE International Conference on Radar, scheduled for October 16-18 in Xi'an, China. Organized under the IEEE Aerospace and Electronic Systems Society (AESS), this conference serves as a primary venue for presenting advancements in radar signal processing and array technologies. These symposia provide the technical validation necessary for private sector adoption of new radar architectures.

Strategic entry checklist for 2026

Entering the radar and AI analytics market in 2026 requires rigorous due diligence. Capital allocation must align with verified technical capabilities and regulatory compliance rather than speculative hype. The following framework guides investors and business leaders through the essential evaluation steps.

Confirm the provenance and latency of input data. In high-stakes environments like missile defense, where the Pentagon allocated $1.98 billion in fiscal 2026 for ground-based radar upgrades, data accuracy is non-negotiable. Ensure the vendor’s data pipeline meets IEEE AESS standards for reliability and precision.

Evaluate the vendor’s machine learning models for real-time pattern recognition. Look for independent validation, such as top scores in Frost Radar reports for cloud runtime security. The AI component must demonstrate measurable improvements in threat detection without introducing systemic vulnerabilities.

Verify adherence to international standards and national security protocols. Participation in official forums like the 2026 CIE International Conference on Radar indicates a commitment to standardized interoperability. Non-compliance with emerging data sovereignty laws can derail deployment timelines.

Require proof of robustness against adversarial conditions. Systems must perform under signal degradation and electronic warfare scenarios. Request case studies from sectors like weather radar meteorology or aerospace, where failure consequences are severe and data integrity is paramount.

Beyond initial acquisition, calculate long-term maintenance and update costs. Legacy system overhauls, such as those mandated for space force infrastructure, reveal hidden expenses in integration and training. Ensure the vendor’s roadmap includes sustainable software updates and hardware support.

| Evaluation Metric | Benchmark | Failure Impact |

|---|---|---|

| Data Latency | <50ms | High |

| AI Accuracy | >99.5% | Critical |

| Compliance | IEEE/DoD | Legal |

Common Questions About Radar Technology

Investors and analysts frequently encounter ambiguity when distinguishing between various "radar" sectors, ranging from aerospace defense to cloud security. Clarifying these definitions is essential for accurate market positioning.

What is the RADAR Challenge 2026?

The RADAR Challenge 2026 is an APSIPA Grand Challenge focused on Robust Audio Deepfake Recognition. Unlike general security benchmarks, this challenge specifically targets robustness under media transformations. It simulates realistic distribution pipelines, including compression, resampling, and noise, to evaluate how well deepfake detection models hold up in real-world audio environments [[src-1]].

How is the Space Force upgrading defense radars?

The Pentagon’s fiscal 2026 reconciliation package allocated $1.98 billion specifically for improved ground-based missile defense radar systems [[src-4]]. This funding supports the overhaul of legacy infrastructure, signaling a strategic shift toward modernizing detection capabilities against emerging aerial threats.

What distinguishes the ARM FY2026 Radar Plan?

The ARM (Atmospheric Radiation Measurement) program released its FY2026 Radar Plan, which outlines data availability schedules and research priorities. The plan notes that 2025 data became available in March 2026, with yearly releases expected in the spring, adjusted based on operational priorities [[src-3]]. This data is critical for climate modeling and atmospheric science.

Is Frost Radar related to defense technology?

No. The "Frost Radar" referenced in market reports is a Gartner-style analyst framework for evaluating technology vendors. For instance, CrowdStrike was named a leader in the 2026 Frost Radar for Cloud Runtime Security, a classification entirely separate from physical radar hardware or defense applications [[src-5]].

No comments yet. Be the first to share your thoughts!